By

By

Last week, we walked through how stock trading works in Kenya — how to open a CDS account, pick a broker, and start buying shares on the NSE. If you read that piece, you already understand the investor's side of the story. But there is another perspective that most people never think about: the company's side.

Here is the question that sparked this article. If Safaricom sells you shares and you later resell them to your friend at a higher price, Safaricom gets none of that extra money. So why on earth does Safaricom care what price you are selling at? Why do companies spend enormous energy trying to keep their share price high when those share transactions stopped putting money in their accounts long ago?

The answer involves a web of incentives, power, and financial mechanics that are fascinating once you see them clearly. And to understand them, we need to go back to the very beginning: the day a company first sells shares to the public.

What Actually Happens During an IPO

When a company "goes public," many people picture the founders selling their entire stake to the world. That is not what happens. During an Initial Public Offering (IPO), companies typically sell only between 10% and 30% of their total shares to the public. This freely traded portion is called the "free float."

There are deliberate reasons for keeping the free float small. Selling fewer shares creates scarcity, which tends to push prices up as demand outstrips supply. It also lets the company test how the public market values them before flooding the market with shares. Additionally, early investors and founders are usually locked in by "lock-up periods" of between 90 and 180 days post-IPO anyway, preventing them from selling their existing shares immediately even if they wanted to.

So who decides the IPO price, and how do they arrive at a number?

The price is not a guess. Investment banks, such as Goldman Sachs or Morgan Stanley, act as "underwriters" and engineer that first number through a meticulous process.

They start with the company's actual financials. Banks look at what the market pays for similar companies, using a metric called the Price-to-Sales (P/S) ratio. If comparable tech companies are trading at 15 to 20 times their annual revenue, the banks apply a similar multiplier to the IPO candidate's revenue to establish a baseline valuation.

Then comes the psychological part. The company and its bankers go on a "roadshow," pitching the stock to large institutional investors such as mutual funds, hedge funds, and pension funds. The bank tells them: "We think the company is worth X, so we want to price the shares at Y. How many shares do you want at that price?" The investors submit bids into a ledger called the "order book." If demand is weak, the price drops. If the book is heavily oversubscribed, the bank knows it can raise the target price.

The night before the stock hits the exchange, the bank locks in the final IPO price. This is the exact price at which institutional investors buy the shares before ordinary retail investors can touch them.

The IPO Pop: When the Real Drama Begins

Here is something most first-time investors do not know: the public almost never gets to buy at the official IPO price.

When the stock market opens the morning after an IPO, a morning auction runs to match retail investors scrambling to buy, with the institutional investors who purchased the night before. If the IPO price was set at KES 100 but millions of people are placing buy orders, a supply-and-demand imbalance pushes the price up.

This is what Wall Street calls the "IPO pop." The official price might be KES 100, but the first trade that flashes on your screen could be KES 140. That gap is pure human psychology and market hype.

To put this in concrete terms: an institutional investor who received shares the night before at KES 100 could theoretically sell them the next morning at KES 140 and pocket KES 40 per share instantly. This is called "flipping," and investment banks strongly discourage it. If a fund flips its IPO shares on day one, the bank will typically bar them from future IPO allocations. Most large investors hold their position for a while, or sell only a small fraction early, to protect their access to future opportunities.

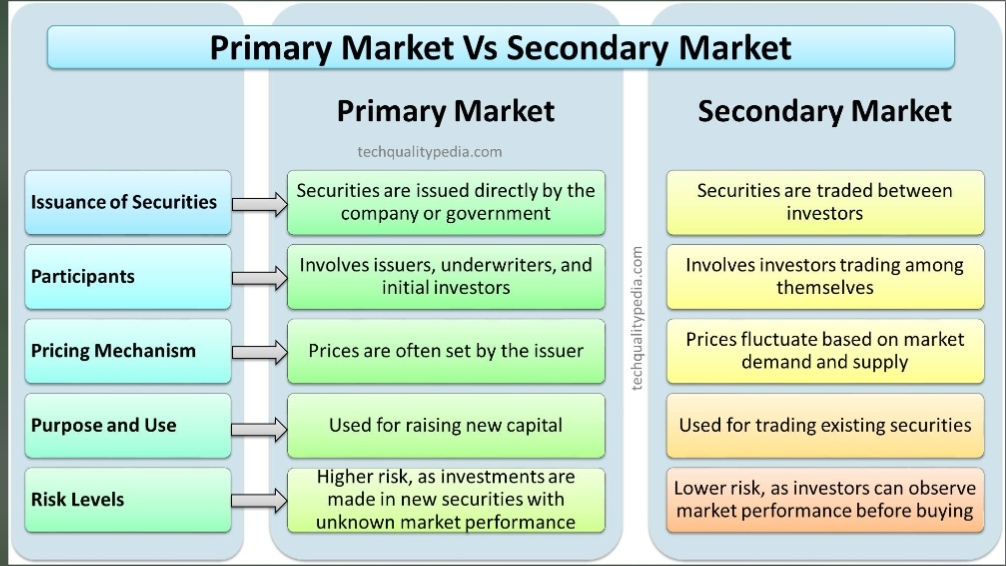

The Primary Market vs. The Secondary Market

This IPO pop introduces one of the most important concepts in understanding how companies relate to their own stock price.

When the company first sells shares to institutional investors at KES 100, that transaction happens in what is called the Primary Market. The company receives that KES 100 per share directly into its bank account to fund its operations. This is when the company actually raises money.

Once the shares start trading publicly on the exchange, every subsequent transaction happens in the Secondary Market. The company is no longer involved. If you buy a share for KES 140 and later sell it to someone else for KES 170, the company's bank account does not change by a single cent. That KES 30 profit goes entirely between the two investors.

This is why the stock market parallel to Apple selling you an iPhone breaks down. Apple does not care what price you resell your phone for because it sold you a product. But a company is selling a piece of itself, and the implications of that never fully go away — even after the initial transaction is done.

So Why Does the Share Price Still Matter to the Company?

Here is where it gets genuinely interesting. There are at least four powerful reasons why companies remain deeply invested in their secondary market stock price, even though those trades no longer directly fund the company.

Executive compensation is tied to it. Most CEOs and top executives do not care much about their base salary, which is often relatively modest. The real money comes from Stock Options and Restricted Stock Units (RSUs). If a CEO is given 1 million shares as a bonus, and the stock is at KES 20, that bonus is worth KES 20 million. If they grow the company and the stock rises to KES 100, that same bonus is worth KES 100 million. This structure aligns the executives' personal wealth directly with shareholders. When the stock crashes, the executives feel it personally.

Future fundraising depends on it. An IPO is never the last time a company raises money from public markets. Companies regularly return to sell more shares to raise additional cash — this is called a secondary offering or follow-on offering. Imagine a company wants to raise KES 1 billion to build a new factory. If their stock is trading at KES 100, they only need to create and sell 10 million new shares. If the stock has crashed to KES 10, they would need to flood the market with 100 million new shares to raise the same amount. That flood of new shares "dilutes" existing shareholders, making them angry, and often causes the price to fall further. A high stock price is essentially a superpower for raising capital efficiently.

Stock is currency for acquisitions. If Anthropic wants to buy a smaller robotics startup for KES 10 billion and its stock is highly valued and easily tradeable, it can simply offer the startup's founders KES 10 billion worth of Anthropic stock instead of cash. The founders will happily accept liquid, valuable shares. A company with a high stock price has a near-infinite acquisition currency that costs it nothing in cash.

A low price invites hostile takeovers. Remember that 10% to 30% of shares floating freely in the public market? If the stock price drops far enough, a rival company or a wealthy investor could quietly accumulate those cheap shares in the secondary market. If the founders ever fall below 51% voting power, a collapsed stock price turns the company into a sitting duck for a hostile buyout. The founders could lose control of something they spent years building.

There is also a reputational dimension. A crashing stock signals to the world that a company may be in trouble. Enterprise clients might worry the company is going under and take their business elsewhere. Suppliers may demand tighter payment terms. The share price functions as a public health report card, and a bad one has real-world consequences.

The Brilliant Trick of Dual-Class Shares

Here is where things get clever. Owning the most shares does not always mean having the most power.

Many modern tech companies — including Meta, Alphabet (Google), and DoorDash — use what is called a dual-class share structure. They split their stock into different classes: Class A shares for the public, carrying one vote each, and Class B shares for founders and early insiders, carrying ten votes or more each.

The numbers on Meta are striking. Mark Zuckerberg holds approximately 13.68% of Meta's equity but commands 61.2% of the total voting power because his Class B shares carry ten votes apiece. He could theoretically sell most of his financial stake in Meta and still single-handedly veto every major decision the company ever makes.

This structure is controversial. The Investor Coalition for Equal Voting Rights, representing $4 trillion in assets, advocates for "one share, one vote," arguing that concentrated power risks misaligned incentives. BlackRock and Vanguard have voted against Meta's dual-class structure at annual meetings, though they are always outvoted by Zuckerberg's bloc.

For companies that do not use dual-class shares, founders almost always lose majority control eventually. Every time a company issues new shares to raise money or grants stock options to employees, the founders' percentage gets diluted. When that dilution pushes them below 51% ownership, control shifts to the Board of Directors, who are elected collectively by all shareholders.

The Long Road to an IPO: How Startups Raise Money in Stages

Before any company reaches an IPO, it lives in the world of private finance. Since private companies cannot sell shares to ordinary people, they rely on Venture Capitalists (VCs) — wealthy investment firms that specialize in funding high-risk, high-growth startups.

This funding comes in structured rounds, each named for how mature the company is.

The Seed Round is the earliest money, often used to hire the first few engineers and build a basic prototype. The company is usually worth very little at this stage, and the amounts are small.

Series A comes when the prototype works and early customers are using it. VCs invest millions to help the company launch commercially.

Series B, C, D, and beyond are scaling rounds. The company is expanding, acquiring competitors, building infrastructure, and pouring resources into growth.

Each round requires the founders to issue brand new private shares to the VCs in exchange for cash. And each round dilutes the founders a little more.

To see how this plays out, consider a simple example. Two founders start an AI company with 1 million shares split evenly. At Series A, a VC values the company at KES 400 million and invests KES 100 million. The post-money valuation is KES 500 million, so the VC owns 20%. To give the VC their 20%, the company prints 250,000 new shares. The founders now each own 40%, diluted from 50%.

At Series B, a bigger VC values the company at KES 2 billion and invests KES 500 million. Everyone gets diluted by another 20%. The original founders now each own 32%, down from 50% at the start.

By the time a startup successfully navigates Seed through Series D and reaches an IPO, it is common for founders to own only 10% to 20% of their company. But here is the key insight: owning a smaller slice of a vastly more valuable company still makes them extraordinarily wealthy. A founder who owns 15% of a company worth KES 500 billion has done incomparably better than someone who owns 100% of a company worth nothing. This is what is sometimes called the "bigger pizza" logic — owning a smaller slice of a much bigger pizza is the whole point.

This is also exactly why founders invest in dual-class shares. Even though they might only own 15% of the financial pie at the IPO, the dual-class structure lets them retain 51% or more of the voting power, preserving their control over the company's direction.

How Anthropic Is Almost Worth a Trillion Dollars Without a Trillion in the Bank

The concept of private valuation confuses a lot of people. When you hear that a company is "worth" nearly a trillion dollars, it does not mean they have that much cash sitting in a vault.

Anthropic, the AI company behind the Claude family of models, is a perfect current example. Anthropic recently reported a $47 billion revenue run rate, up from a $30 billion run rate earlier this year and $10 billion in annual revenue last year. The newest funding round almost tripled Anthropic's valuation from February, when it was worth $380 billion.

That valuation is not stored anywhere. It is simply what investors believe the entire company would be worth if you could buy 100% of it today. They looked at Anthropic's explosive revenue growth, its dominance in enterprise AI and coding tools, and its potential to capture a massive share of the AI market, and concluded that buying the whole company right now would theoretically cost nearly a trillion dollars.

What makes this remarkable is the speed of the climb. At the beginning of 2025, Anthropic's run-rate revenue had grown to approximately $1 billion. By August 2025, just eight months later, it reached over $5 billion, making Anthropic one of the fastest-growing technology companies in history. The valuation has followed that trajectory, ballooning from $61.5 billion in early 2025 to nearly $1 trillion today.

When Dilution Works for You: The Dividend Maths

Creating new shares and diluting existing shareholders is not always a bad thing. The difference is what the money gets used for.

If a company creates new shares just to cover losses or fund wasteful spending, investors see their ownership percentage shrink while the company does not get more valuable. That is destructive dilution.

But consider a company that creates 10 million new shares to fund a factory that dramatically expands its revenue. Before the factory: there are 10 million shares, you own 1 million (10%), and the company pays out a total annual dividend of KES 1 million, giving you KES 100,000. After creating 10 million new shares to build the factory: there are now 20 million shares, your 1 million represents only 5%, but the factory's success triples the company's profits, so the total dividend payout grows to KES 6 million. Your 5% now pays you KES 300,000. Your ownership percentage got cut in half, but your actual income tripled.

This is why investors are far less concerned about dilution itself and far more focused on what the dilution is funding.

The opposite also happens. When companies have excess cash, they can do what is called a share buyback: going into the secondary market and purchasing their own shares, then cancelling them. Apple and Alphabet have spent hundreds of billions of dollars doing this. If there were 10 million shares and the company buys back 2 million, your 1 million shares suddenly jump from representing 10% of the company to 12.5%, without you spending anything. Each remaining share becomes more valuable automatically.

What Happens to Employees at an IPO

For early employees at a startup, the IPO can be genuinely life-changing. When you join a young company, you are typically not given actual shares immediately. Instead, you receive Stock Options — a contract granting you the right to buy a certain number of shares in the future at a locked-in, heavily discounted price called the "strike price."

The logic is simple. If you join a startup early and your strike price is locked at KES 50 per share, and the company goes public five years later with shares trading at KES 1,000, your profit per share is KES 950. If you hold 50,000 options, your total windfall is KES 47.5 million. This is executed through what is called a "cashless exercise," where a broker simultaneously buys and sells the shares so you never need to produce the KES 50 purchase price out of your own pocket.

But there is a serious risk. This entire calculation depends on the company's value going up. If the IPO price is lower than your strike price — for example, the stock trades at KES 30 on the public market but your strike price is KES 50 — your options are "underwater." No rational person would pay KES 50 to buy something worth KES 30 on the open market. The options become worthless paper. This is the ultimate gamble of joining a startup early: enormous upside, but genuine risk of getting nothing.

The Institutions Nobody Talks About

When we imagine stock market activity, we picture individual investors on trading apps. In reality, the real power sits with institutional investors. Firms like BlackRock, Vanguard, and State Street collectively manage over $20 trillion in assets and hold the massive blocks of shares that actually move markets.

If a company wants to do a secondary offering to build a new factory, the CEO does not ask the general public for permission. They get on a private plane, fly to meet portfolio managers at Vanguard or BlackRock, and pitch the plan. If those firms say yes, the capital raise happens. If they say no, the plan collapses. The decision-making weight of a few institutional investors dwarfs that of millions of individual retail shareholders combined.

The Full Picture

The stock market looks simple from the outside: prices go up, prices go down, people make money or lose it. But beneath that surface is an intricate system where companies, founders, employees, VCs, investment banks, and institutional investors all operate with their own incentives, time horizons, and strategies.

Understanding this from the company's perspective helps explain behaviour that otherwise seems irrational. Why does a company that has already raised its money care about secondary market prices? Because those prices determine executive compensation, future fundraising power, acquisition ability, and survival against takeover threats.

The share price is not just a number on a screen. For the people running these companies, it is a measure of credibility, a tool for growth, and sometimes, the thing standing between them and losing everything they built.

Comments